![]()

This package is in Technical Preview Stage: The API is stabilizing and tests are passing but it has not been used in practice for very long. Please report any issues, provide feedback, and request specific features using the Discussions or Issues in this repository.

Interested in developing economic scenario generators in Julia? Consider contributing to this package. Open an issue, create a pull request, or discuss on the Julia Zulip's #actuary channel.

EconoicScenarioGenerators.jl is now available via the General Registry. Install and use in the normal way:

- Add EconomicScenarioGenerators via Pkg

import EconomicScenarioGeneratorsorusing EconomicScenarioGeneratorsin your code

First, import both EconomicScenarioGenerators and FinanceModels:

using EconomicScenarioGenerators

using FinanceModels

VasicekCoxIngersolRossHullWhite

BlackScholesMerton

m = Vasicek(0.136,0.0168,0.0119,Continuous(0.01)) # a, b, σ, initial Rate

s = ScenarioGenerator(

1, # timestep

30, # projection horizon

m, # model

)You can collect a single generated scenario lik so:

rates = collect(s)And the package integrates with FinanceModels.jl:

YieldCurve(s)

will produce a yield curve object:

⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀Yield Curve (FinanceModels.Yield.Spline)⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀

┌────────────────────────────────────────────────────────────┐

0.04 │⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│ Zero rates

│⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⠀⠀⠀⠀⠀⠀⠀⠀⡀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⠀⠀⠀⠀⠀⠀⡠⠎⠉⠉⠊⠉⠑⠦⠤⠤⣄⡀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⣀⣀⡠⠤⠤⠔│

│⠀⠀⠀⠀⢀⠖⠁⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠉⠑⠦⢄⣀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⢀⣀⣀⣀⠤⠔⠒⠊⠉⠉⠀⠀⠀⠀⠀⠀│

│⠀⠀⠀⢰⠃⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠉⠓⠒⠦⠤⢄⣀⠀⠀⠀⠀⠀⠀⠀⠀⣀⣀⠤⠔⠒⠉⠉⠁⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⠀⠀⠀⡎⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠉⠒⠒⠒⠒⠊⠉⠉⠁⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

Continuous │⠀⠀⢰⠁⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⠀⠀⡇⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⠀⡸⠁⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⢀⡇⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⡸⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

│⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉⠉│

│⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

-0.01 │⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀│

└────────────────────────────────────────────────────────────┘

⠀0⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀time⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀30⠀

A CIR model:

m = CoxIngersollRoss(0.136,0.0168,0.0119,Continuous(0.01))Construct a yield curve and use that as the arbitrage-free forward curve within the Hull-White model.

using FinanceModels, EconomicScenarioGenerators

rates =[0.01, 0.01, 0.03, 0.05, 0.07, 0.16, 0.35, 0.92, 1.40, 1.74, 2.31, 2.41] ./ 100

mats = [1/12, 2/12, 3/12, 6/12, 1, 2, 3, 5, 7, 10, 20, 30]

curve = FinanceModels.fit(

Spline.Cubic(),

CMTYield.(rates,mats),

Fit.Bootstrap()

)

m = HullWhite(.1,.002,curve) # a, σ, curve

s = ScenarioGenerator(

1/12, # timestep

30., # projection horizon

m, # model

)Create 1000 yield curves from the scenario generator:

n = 1000

curves = [YieldCurve(s) for i in 1:n]

```julia

Plot the result:

```julia

using Plots

times = 1:30

p=plot(title="EconomicScenarioGenerators.jl Hull White Model")

# plot the zero rates

for d in curves

plot!(p,times,rate.(zero.(d,times)),alpha=0.2,label="")

end

plot!(times,rate.(zero.(curve,times)),line=(:black, 5), label="Given Yield Curve")

p

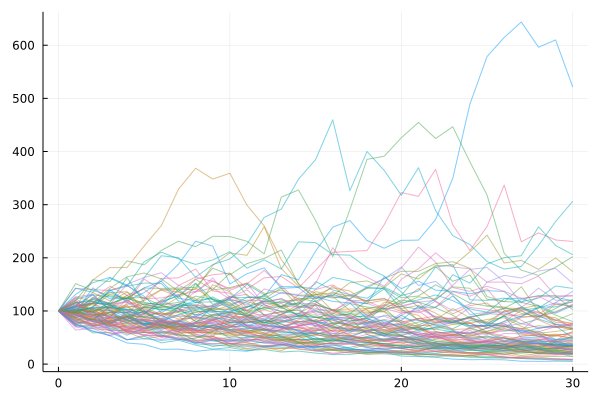

m = BlackScholesMerton(0.01,0.02,.15,100.)

s = ScenarioGenerator(

1, # timestep

30, # projection horizon

m, # model

)Instantiate an array of the projection with collect(s).

Plot 100 paths:

using Plots

projections = [collect(s) for _ in 1:100]

p = plot()

for p in projections

plot!(0:30,p,label="",alpha=0.5)

end

p

Combined with using Copulas, you can create correlated scenarios with a given copula. See ?Correlated for the docstring on creating a correlated set of scenario generators.

Create two equity paths that are 90% correlated:

using EconomicScenarioGenerators, Copulas

m = BlackScholesMerton(0.01,0.02,.15,100.)

s = ScenarioGenerator(

1, # timestep

30, # projection horizon

m, # model

)

ss = [s,s] # these don't have to be the exact same, but do need same shape

g = ClaytonCopula(2,7) # highly dependendant model

c = Correlated(ss,g)

x = collect(c) # an array of tuples

using Plots

# get the 1st/2nd value from the scenario points

plot(getindex.(x,1))

plot!(getindex.(x,2))