| layout | title | date | comments | categories | language | slides |

|---|---|---|---|---|---|---|

post |

Designing Stock Exchange |

2019-08-12 09:50 |

true |

system design |

en |

false |

- order-matching system for

buyandsellorders. Types of orders:- Market Orders

- Limit Orders

- Stop-Loss Orders

- Fill-or-Kill Orders

- Duration of Orders

- high availability and low latency for millions of users

- async design - use messaging queue extensively (btw. side-effect: engineers work on one service pub to a queue and does not even know where exactly is the downstream service and hence cannot do evil.)

Reverse Proxy

API Gateway

Order Matching

User Store

settle

Orders

Stock Meta

auth

Cache

Balances & Bookkeeping

external pricing

clearing

house

house

Bank, ACH, Visa, etc

Payment

Audit & Report

- shard by stock code

- order's basic data model (other metadata are omitted):

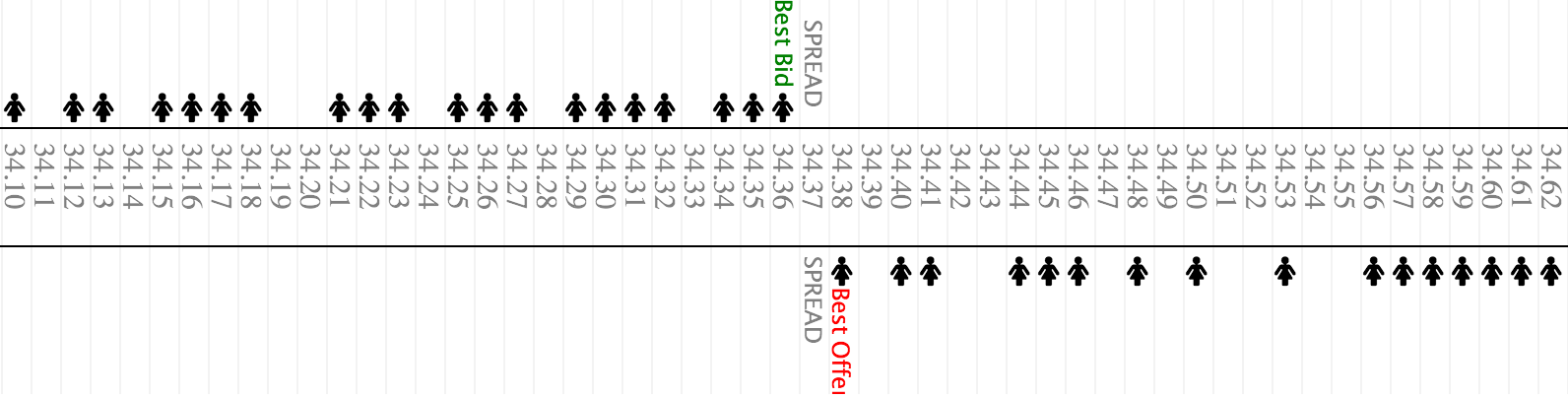

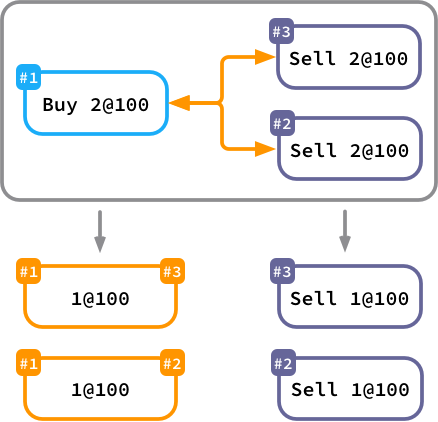

Order(id, stock, side, time, qty, price) - the core abstraction of the order book is the matching algorithm. there are a bunch of matching algorithms(ref to stackoverflow, ref to medium)

- example 1: price-time FIFO - a kind of 2D vector cast or flatten into 1D vector

- x-axis is price

- y-axis is orders. Price/time priority queue, FIFO.

- Buy-side: ascending in price, descending in time.

- Sell-side: ascending in price, ascending in time.

- in other words

- Buy-side: the higher the price and the earlier the order, the nearer we should put it to the center of the matching.

- Sell-side: the lower the price and the earlier the order, the nearer we should put it to the center of the matching.

x-axis

with y-axis cast into x-axis

Id Side Time Qty Price Qty Time Side

---+------+-------+-----+-------+-----+-------+------

#3 20.30 200 09:05 SELL

#1 20.30 100 09:01 SELL

#2 20.25 100 09:03 SELL

#5 BUY 09:08 200 20.20

#4 BUY 09:06 100 20.15

#6 BUY 09:09 200 20.15

Order book from Coinbase Pro

The Single Stock-Exchange Simulator

- example 2: pro-rata

How to implement the price-time FIFO matching algorithm?

- shard by stock, CP over AP: one stock one partition

- stateful in-memory tree-map

- periodically iterate the treemap to match orders

- data persistence with cassandra

- in/out requests of the order matching services are made through messaging queues

- failover

- the in-memory tree-maps are snapshotting into database

- in an error case, recover from the snapshot and de-duplicate with cache

How to transmit data of the order book to the client-side in realtime?

- websocket

How to support different kinds of orders?

- same

SELL or BUY: qty @ pricein the treemap with different creation setup and matching conditions- Market Orders: place the order at the last market price.

- Limit Orders: place the order with at a specific price.

- Stop-Loss Orders: place the order with at a specific price, and match it in certain conditions.

- Fill-or-Kill Orders: place the order with at a specific price, but match it only once.

- Duration of Orders: place the order with at a specific price, but match it only in the given time span.

- Preserves all active orders and order history.

- Writes to order matching when receives a new order.

- Receives matched orders and settle with external clearing house (async external gateway call + cronjob to sync DB)

- How Exchange Happen? Simulating a financial exchange in Scala

- Open Sources

- The Financial Information eXchange ("FIX") Protocol

- Types of orders: Technical Analysis Course. Training,Coaching & Mentoring for Traders / Investors - Types of orders used when buying or selling a stock

- GitHub - fmstephe/matching_engine: A simple financial trading matching engine. Built to learn more about how they work.

- Automated Algorithmic Trading: Learning Agents for Limit Order Book Trading